We all use credit cards for various reasons, to buy groceries, for bill payments and for shopping, but what if I say you can save money using your credit card?, Yes, it is true you can save a little money by following simple tips as per below.

Guide to Save Money using Your Credit Card

With the rise of plastic money, many people often use credit/debit cards to pay off their bills or to make some sort of purchases. In many ways using credit cards is convenient, because you don’t have carry physical money all the time.

Thought we have multiple benefits using credit cards, many people argue that excessive use of credit cards will tend to mislead us, and sometimes you will get tempted to buy products that you really don’t need.

First, let’s understand, unlike any other financial product Credit cards are also comes with various pros and cons. It is absolutely your responsibility to educate yourself on how to use Credit card to get benefited.

So, saving money using a credit card is still possible, I’ve done that (even now I’m doing) practically, maybe you also can do that by following below tips.

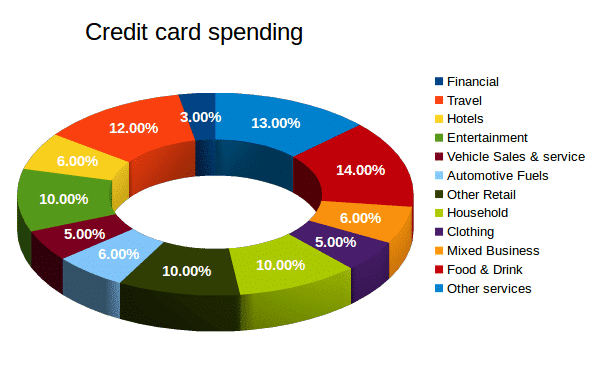

Do you know these facts about credit card spending?

I’ve analyzed last 12 months “The UK card association” data (Jan’14 to Jan’15) to identify in which category most of the people have been spending money using their credit cards. As per my analysis I’ve found below interesting facts.

-

14% on Food & Drink

-

13% on Other Services

-

12% on Travel

-

10% on Entertainment

So, under which category are you spending?

Without further delay, here is my 5 ways to save money using credit card.

1) Radical change in marketing & digital payment systems

Mobile applications have brought radical change in our lifestyle, there were days when we thought Computers are the best invention made by the human being, but now, I think its mobiles!!!

Well, If you notice closely, from past 2 to 3 years, many small and medium companies have been started spending their marketing budget directly to consumers with ‘cash back offers’, so why can’t you take full advantage of that..?

It’s very simple; do you have any upcoming bill payments? if so, you need to spend some time over the Internet searching for any offers related to your payment. Most of the times Credit cards & digital wallets come up with some exciting offers.

My experience:

#1 by using HDFC credit card I have saved 5% on my insurance premium (Rs. 10,650 *5% = Rs. 532.5), it was one of their promotional offer on bill payment system, so at the end of the day I’ve been (customer) benefited by saving Rs. 532.

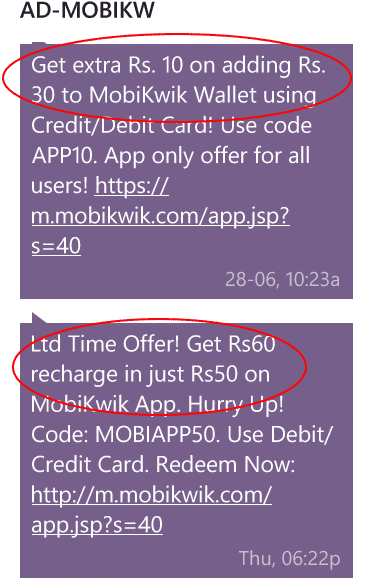

#2 From past one year I’ve been started using digital wallet services like Mobikwik, Paytm & Freecharge to make my bill payments. Interestingly, they’ve been offering cash backs when you add money using credit/debit cards to their wallets, even sometimes when you pay using their wallets.

Have a look at below promotional message that I’ve received from Mobikwik.

Cash back offers may vary from 10% to 60%, depends on what type of payment that you are making. There were days when I’ve received 100% (25 to 25) cash back on my mobile recharge also.

2) Re-think your spending and save money based on past data

Credit cards are not only useful to make some sort or purchases, but you can also use indirectly to save some money by analyzing your monthly spending data. Not sure how to do that? No problem, here we have simple steps to help you understand.

Step #1 Login to your credit account and download last six months spending data in excel file

Step #2 Start analyzing your past expenses and categorize them as daily needs or wants (for example, purchasing Apple iphone is want, at the same time purchasing budget phone for daily requirements is a need)

You may refer my other article about tips to create wonderful reports in excel by using simple formulas & inbuilt options.

Step #3 Once you completed analyzing, sum your expenses by needs and wants and try to see in which category you’ve been spending.

Step #4 Now that you have your past spending data, it’s time to cut down all the unnecessary expenses based on the past events.

With this I recall one of the famous quote from Warren Buffett “If you buy things you don’t need, you will soon sell things you need”.

3) Use reward credit cards

As per American bankers association, 83% users at least have one rewards card with them, which means there is a lot of space around rewards program.

As a part of marketing efforts most of the banks are currently offering various reward cards to attract customers. To give you more information, banks will have tie-ups with various merchants like Restaurants, Hotels & Online Marketing giants.

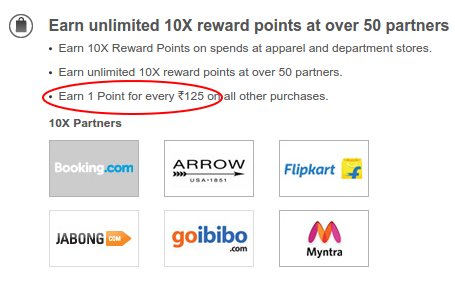

Here is one of the reward card promotion from citibank

When you make a purchase using their card you will be offered some reward points, you can use these points either to make new purchases or to pay off some portion of your bill.

I’m currently using Citibank Indian oil Credit card, If I make any purchases using this card, my account will be credited with some reward points. Once I have 150 reward points I can use those to fill Fuel.

4) Make use of interest factor

Most of us doesn’t pay much attention to this, but believe me this point is going to be your favorite one, when you use it appropriately.

But the catch here is, how well you leverage 45 day repayment period to take interest factor advantage, still confused? Ok, here is an example.

Mr. X has to pay Rs. 30,000 insurance premium in next month cycle, So he’ll make a payment with his credit card to take some advantage.

Points he has to consider:

-

Since most of the insurance companies will offer one month grace period for premium payment, Mr. X will make a payment exactly next day after credit card bill generation date (not possible in all the cases, but you can try).

-

Now Mr. X has 45 days time to repay his credit card bill

-

Mr. X will transfer his 30,000 cash to Saving Bank account where he can earn 4% interest p.a.

-

By doing this he will earn Rs.150 interest + few reward points

-

And after 45 days he will repay the full credit card bill with the money that he has saved in SB account

Read also: 8 Tips To Reinvent Your Job Skills List And Win In Your Next Interview

5) Shop online with your credit card

According to Myles Anderson from brightlocal.com, 37% of small & medium business are plan to spend more on internet marketing in 2015, & 32% of them say internet marketing is very effective at attracting customers.

Currently the online shopping/internet marketing industry is in boom, The model itself has a big cost advantage. The seller doesn’t have to open physical store, so he can save a lot of money on Rent.

If you observe closely, many big giants have been started competing with each other (for example flipkart & Amazon in India) . So the big strategy for them to attract customers is to adopt win win strategy.

Win Win is a pretty simple strategy, where online shopping companies will have tie-up’s with leading banks to provide discounts on product purchases, so banks will get more and more transactions along with an opportunity to acquire new customers.

Often times you’d have seen many add banners about 10% additional discounts when you make a purchase with their credit cards.

So at the end of the day customer will get benefited out of all the promotional offers, and with the online shopping model.

Catch here

Discounts and promotional offers look very attractive and often times you’ll be motivated to buy unwanted things. To avoid this better do not go for window shopping.

6) (Bonus tip) go for zero annual fee card and use it for emergency

Since we don’t have any control on emergencies, we should be prepared for that by saving some money as an emergency fund. At the same time it’s a good idea to have at least one credit card (preferably zero annual fee card, if you intend to use only for emergencies), to offset some portion of your expenses.

Flip side of the coin: why credit cards are bad?

Credit cards can be very dangerous, if you don’t know how to use it. The most basic problems are, high charges if you don’t re-pay on time, annual maintenance fee & higher interest rate vs personal loan.

I’ve few more tips below, on how to use credit cards.

1) Use it wisely

Most of the online promotional offers may tend to mislead and make you buy unwanted things. Better be careful with online promotions, and buy products or services only if you desperately need them.

Tip: Don”t keep credit card in your wallet, instead keep it in your home, use it only when you need.

2) Pay on time

Credit cards can be very unpleasant, when you don’t make your re-payments on time. Often times you will be charged high penalties for late payments along with high interest rates.

Tip: Better link your credit card to bank account and put a standing instruction to process payment automatically.

3) Do not withdraw money

You will have an option to withdraw some money using your credit card for urgent needs. But it is always advisable, not to withdraw money, since bank can levy lot of hidden charges.

Tip: Better borrow money from your friends if you’re in a need, but do not withdraw money

4) Don’t go for more than two cards

Having one card is good and the second card is better (only as a backup), but more than that is not acceptable. It is very hard to manage multiple cards, especially to track your expenses.

Tip: Don’t just through away your third card, instead send out a letter for closing your unwanted cards.

5) Be within credit limit

Every card comes with a certain amount of credit limit based on credit or repayment history. If you exceed your credit limit then you will be charged some amount as a penalty.

Tip: Examine your spending & credit limit often, don’t trap into easy EMI options and make other purchases. Say no to more credit limit.

6) Security – is your credit card in safe hands

Around two to three years back there was a big problem with the credit cards, i.e. no PIN security for authorizing transactions. If you think you still have that type of card, better be aware of possible risks.

Recently we have seen an Ebay website have been hacked and they have stolen all the user information.

Tip: Go for PIN secured credit cards and do not save your card details on any of the online shopping websites.

Conclusion:

Credit cards can be very dangerous when you don’t know how to use, at the same time it can be helping hand when you’re in a trouble. So it is up to you how well you use your credit card to reap better results.

Saving money using credit your card is still possible with a systematic approach, so go ahead and try with confidence.

In my opinion, having at least one card is not a bad idea, but having said that you need to know the basics before you use. Let me know what do you think..!!